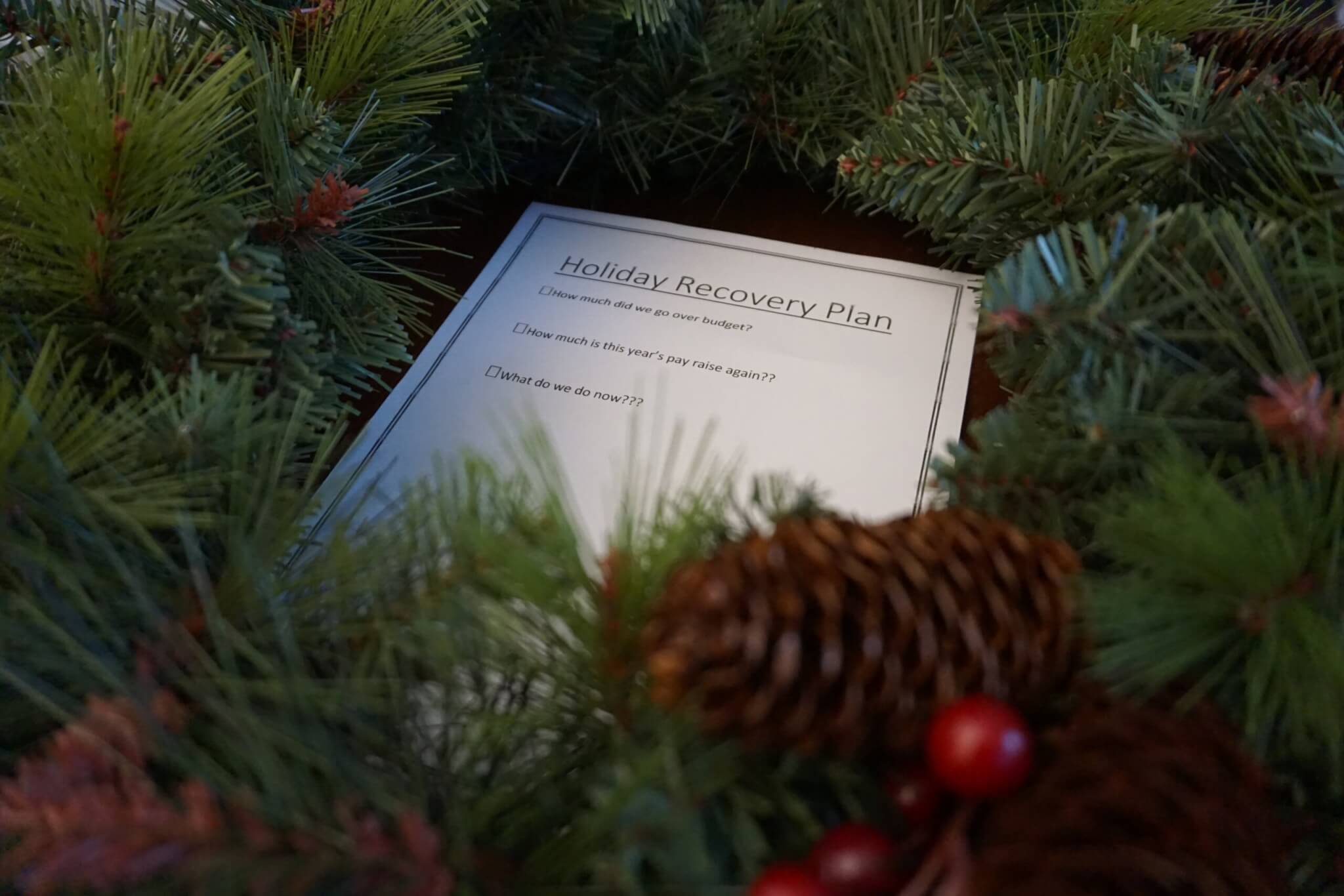

Holiday debt can linger well into 2025, according to results from a new survey, as consumers reveal this year to be a “top financially challenging year.”

The study, conducted by Achieve, shows the average American will spend $2,000 this holiday season. Categories like travel and “putting on” the holidays rank at the top of the costliest areas. This time of year can be stressful without even thinking about money. However, many of us understand the aftermath of holiday [over]spending all too well. So, what should you do now?

Assess the damage

I like to gather data first before dealing with emotions. If you know you overspent, you need to measure how much so you can make adjustments for next year. Start by looking at your credit card balances, noting any savings accounts you “borrowed” from, and writing it down.

If you can’t immediately pay these back, that’s your overage amount. You’ll need to make this up quickly. Not only will interest start to accrue on credit cards, but every extra day you take to pay off last year’s spending, is less time to save for this year. In other words, you can accidentally set yourself up for an even harder time next year.

Break the overspending cycle

The easiest way to break the overspending cycle is to save up throughout the year in a high-yield savings account (HYSA). Tally up everything you spent this past holiday season, divide that by 10, and set up a monthly automatic transfer into your “Holiday Account” for this year.

You might be thinking that sounds all fine and dandy, but where’s this “extra” money coming from? I have a few ideas.

Use pay raises

Luckily, we get an annual pay raise right after the holidays. If you’re smart with your pay raises, you can very quickly bump up your savings and debt paydown rate.

You should enjoy some of your pay raise. However, if you already overspent, you’re paying back past enjoyment. If you get things set up now, you can avoid having to make up lost ground next year.

Using tax return money

If you usually get a refund from filing your tax return each year, you could use this to recover. Getting a big refund might not always be a good thing because it means you gave Uncle Sam an interest-free loan throughout the year. Instead, you could have been saving that money and earning interest yourself.

TIP: You can file your taxes for free using MilTax or the IRS FreeFile program (subject to income limits).

Finding ways to save money

You can always cut your spending. However, this might not be much fun. We recalibrate our budget every year on “Money Day” to find ways to save and adjust our budget. Even trimming $50/month can make a difference.

Actually, I have a free 3-Day Saver’s Challenge to help brainstorm some ideas on how to save money. You can look for discounts, shop around for car insurance, check for cheaper internet service, or cut back on your streaming services for a while. There are many ways to save.

Getting help is, well, helpful

If you’re truly running up against some difficult times, don’t struggle alone. The DOD has many resources to help you out. I’ve met so many wonderful financial counselors over the years. It would be a shame if their expertise went unused.

You can use the Military OneSource website to find a financial counselor, couples counseling, discounts, and so much more. Make sure you use all the benefits you’ve earned through military service!

The bottom line

No matter what situation you find yourself in after the holidays, you can chart a path forward. If you’re feeling the pain right now, take note and make a plan to never feel this way again!

Visit https://enlistedmoney.com for more tips and resources from The Enlisted Money Guy™